Most rejections happen due to a handful of fixable reasons. Understand what went wrong — and how to come back stronger.

The Root Causes

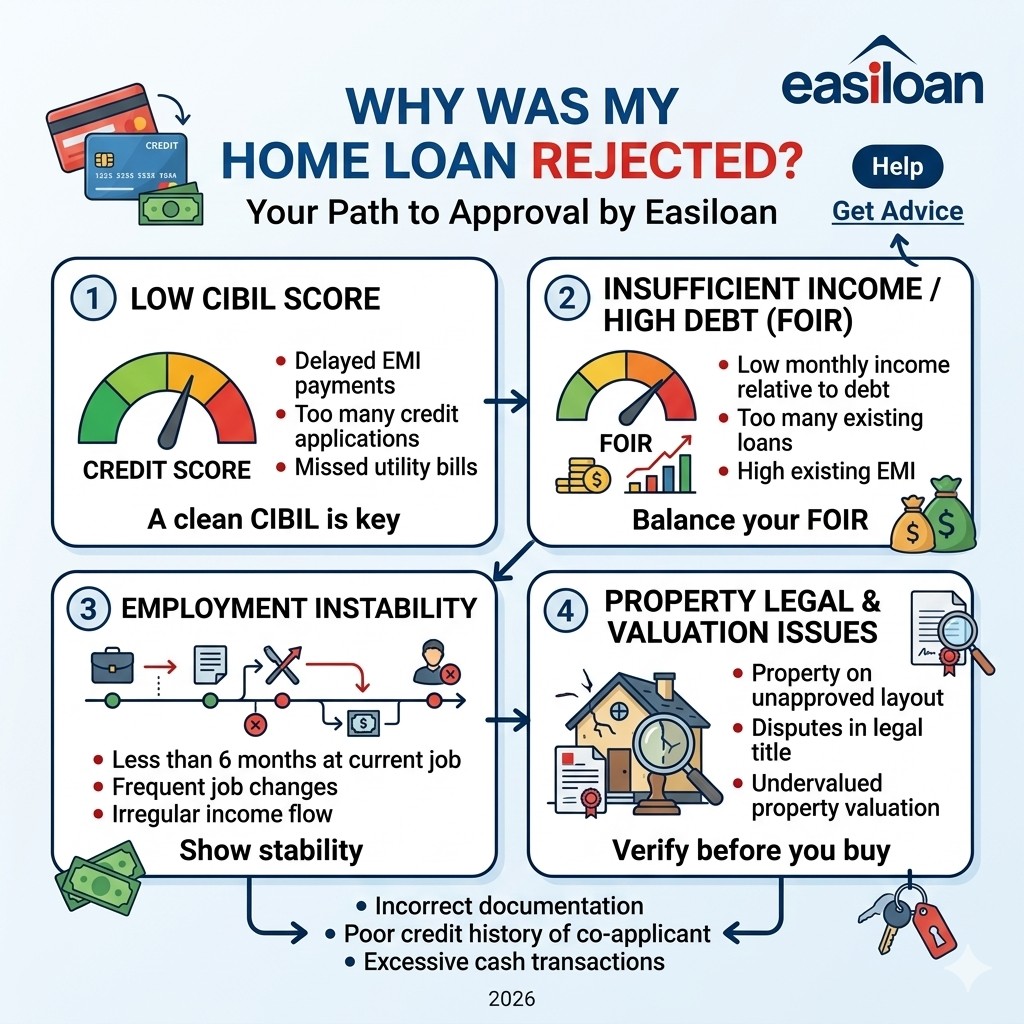

Why Do Home Loans Get Rejected?

Low Credit Score (CIBIL Score)

Your credit score is the first thing every lender checks. A score below 700 significantly reduces your chances of approval.

⚠ Why it happens

- Missed EMIs or credit card payments

- High outstanding debt

✓ How to fix it

- Pay all dues on time

- Avoid multiple loan applications

- Keep credit utilization below 30%

Insufficient Income or Unstable Earnings

Lenders want confidence that you can repay comfortably. Irregular or low income raises serious flags — especially for self-employed individuals.

⚠ Why it happens

- Low monthly income

- Irregular / seasonal income

✓ How to fix it

- Add a co-applicant (spouse / family)

- Show additional income sources

- Apply for a lower loan amount

High Existing Debt (FOIR Issue)

FOIR (Fixed Obligation to Income Ratio) measures what share of your income is already committed to other EMIs. A high FOIR leaves little room for a new home loan.

⚠ Why it happens

- Too many ongoing loans

- Heavy existing EMI burden

✓ How to fix it

- Close small loans before applying

- Avoid taking new credit

- Increase income proof

Employment Instability

Frequent job changes signal financial instability to lenders. Most banks want to see at least 6–12 months of continuity at your current employer.

⚠ Why it happens

- Less than 6–12 months in current job

- Unstable employment history

✓ How to fix it

- Stay in current job longer before applying

- Provide a strong employment record

Property-Related Issues

Sometimes it's not your profile — it's the property. Legal disputes or unapproved layouts (manual khata, Lal Dora, Power of Attorney) can block a loan entirely.

⚠ Why it happens

- Legal issues in property documents

- Unapproved property layouts

✓ How to fix it

- Verify property documents beforehand

- Choose lender-friendly properties

- Work with specialists in such cases

Poor or Incomplete Documentation

Even a strong profile can be rejected for something as simple as a missing document or an error in the application form.

⚠ Why it happens

- Missing income proof

- Errors in application

✓ How to fix it

- Double-check all documents

- Keep bank statements, ID & property papers ready

Your Action Plan

What To Do Immediately After Rejection

Don't Panic — Find the Reason First

Request a written reason from your lender. Understanding the exact cause is step one.

Work on Your Credit Score

Pay overdue amounts, reduce credit utilization, and avoid new applications.

Reduce Existing Debt

Close smaller loans and limit your EMI-to-income ratio before reapplying.

Wait 3–6 Months Before Reapplying

Multiple loan applications in quick succession hurt your credit score further.

Choose the Right Lender for Your Profile

Not every lender uses the same criteria. Flexible lenders can work with informal income, self-employment, and non-standard properties.

Expert Advice

Pro Tips to Boost Approval Chances

Maintain a CIBIL score above 700 consistently.

Keep your total EMI obligations low relative to income.

Apply for a realistic loan amount you can comfortably service.

Add a co-applicant to strengthen your eligibility.

Choose a lender that truly understands your income type.

Rejected by a Traditional Bank? We Can Help.

Easiloan offers flexible eligibility assessment for first-time buyers, self-employed professionals, and those with informal income — where standard banks fall short.

Check Your Eligibility →This article is for informational purposes only and does not constitute financial advice.