Understanding the difference between India's four major credit bureaus — CIBIL, Experian, Equifax, and CRIF High Mark — is essential when applying for a home loan. Each bureau may show slightly different scores based on its data sources and scoring model, and lenders often consult more than one before making a decision.

What Are Credit Bureaus in India?

Credit bureaus in India are organisations that collect and maintain records of borrowers' credit behaviour — loans, repayments, and credit card usage. This data is used by lenders including Housing Finance Companies (HFCs) and NBFCs to assess an applicant's repayment capacity and risk profile.

These bureaus operate under the framework set by the Reserve Bank of India and the Credit Information Companies (Regulation) Act. While they differ in scoring models and data sources, their primary role remains the same: providing reliable credit information to support lending decisions.

The Four Major Credit Bureaus

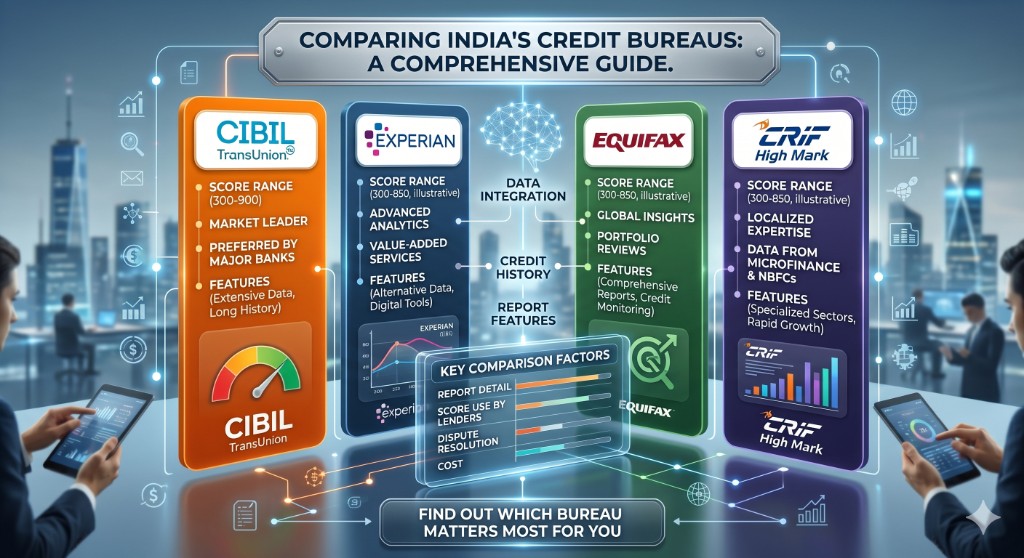

CIBIL (TransUnion)

Widely used by lenders, assigns scores based on repayment history, credit utilisation ratio, and loan enquiries — a key reference during underwriting.

Experian India

Uses its own scoring model and data sources, offering an additional perspective on credit behaviour and repayment patterns across financial institutions.

Equifax India

Focuses on detailed credit data and is often used by lenders for credit report verification during home loan application processing.

CRIF High Mark

Commonly used by lenders including microfinance institutions, it captures data from a wide range of borrowers — including those new to credit.

Key Differences at a Glance

| Parameter | CIBIL | Experian | Equifax | CRIF High Mark |

|---|---|---|---|---|

| Score Range | 300 – 900 | 300 – 900 | 300 – 900 | 300 – 900 |

| Scoring Model | Proprietary, widely accepted | Independent algorithms | Global framework adapted for India | Tailored for retail & microfinance |

| Data Sources | FIs, HFCs, NBFCs, card issuers | FIs, HFCs, NBFCs | FIs, HFCs, NBFCs | FIs, HFCs, NBFCs, MFIs |

| Lender Usage | Most widely used | Cross-checking | Verification | Emerging segments |

| Report Format | Detailed with history & score | Behavioural insights | Risk indicators | Broader borrower segments |

Which Score Do Lenders Prefer?

Many lenders in India primarily look at the CIBIL score due to its wide acceptance and long-standing use in the lending ecosystem. However, lenders may also review reports from Experian, Equifax, or CRIF High Mark to get a more complete view of your credit behaviour.

A broader credit bureau comparison allows lenders to cross-check information, identify inconsistencies, and assess repayment patterns across different data sources — leading to more informed lending decisions.

How Credit Scores Affect Home Loan Approval

Approximate impact of credit score bands on home loan outcomes:

*Indicative approval likelihood. Actual approval depends on income, liabilities, property value, and lender policies.

Tips to Maintain a Strong Credit Score

- Pay all EMIs and credit card dues on time — consistent on-time payments are the single biggest driver of a healthy credit score.

- Keep your credit utilisation below 30% of your available credit limit across all cards and revolving facilities.

- Avoid making multiple loan or credit card enquiries in a short window — each hard inquiry can shave points off your score.

- Maintain a healthy mix of secured (home/auto loans) and unsecured (personal loans/credit cards) credit for a stronger profile.

- Review your credit reports from all four bureaus at least once a year to catch and correct discrepancies before applying.

- Monitor scores across CIBIL, Experian, CRIF, and Equifax consistently — lenders may check any one of them.

Frequently Asked Questions

What is the difference between CIBIL, Experian, Equifax, and CRIF?▾

All four bureaus use similar score ranges (300–900) but differ in data sources, scoring models, and report formats. These differences can lead to slight score variations, though all aim to assess overall creditworthiness.

Which credit score do lenders check for home loans in India?▾

Most lenders primarily check the CIBIL score for home loans, but they may also review Experian, Equifax, or CRIF reports to gain a more comprehensive understanding of your credit profile.

What credit score is required for a home loan in India?▾

A credit score of 700 or above is generally considered suitable for home loans. Meeting this threshold improves approval chances and may help you secure more favourable interest rates and loan terms.

Can lenders check multiple credit bureaus for home loan approval?▾

Yes, lenders can and do check reports from multiple credit bureaus during home loan approval. This helps them verify information and assess your repayment behaviour across different data sources.

Do all credit bureaus show the same credit score?▾

No. Credit scores may vary slightly across bureaus due to differences in data collection and scoring methods. However, the overall trend in your credit behaviour should remain consistent across all platforms.

How often should I check my credit reports?▾

It is advisable to check your credit reports at least once a year from each bureau. Regular monitoring helps identify errors, track improvements, and ensure your credit profile is accurate before applying for a loan.

Ready to apply for a home loan?

Check your credit score, plan repayments with our EMI calculator, and compare lenders after checking eligibility.

This article is for informational purposes only and does not constitute financial advice.