Looking to apply soon? Compare lenders after checking your loan amount eligibility to make a confident choice.

Every year, many borrowers celebrate loan approval and then discover that the credited amount is lower than what the sanction letter showed. The gap between sanctioned amount and disbursed amount is one of the most misunderstood parts of home financing.

This guide explains why lenders approve higher ceilings, why tranches are common in under-construction projects, why sanction-to-payout gaps happen, why some sanctioned loans are never disbursed, and how your outstanding balance evolves separately from sanctioned figures.

The Core Difference, Explained Simply

Approval Stage

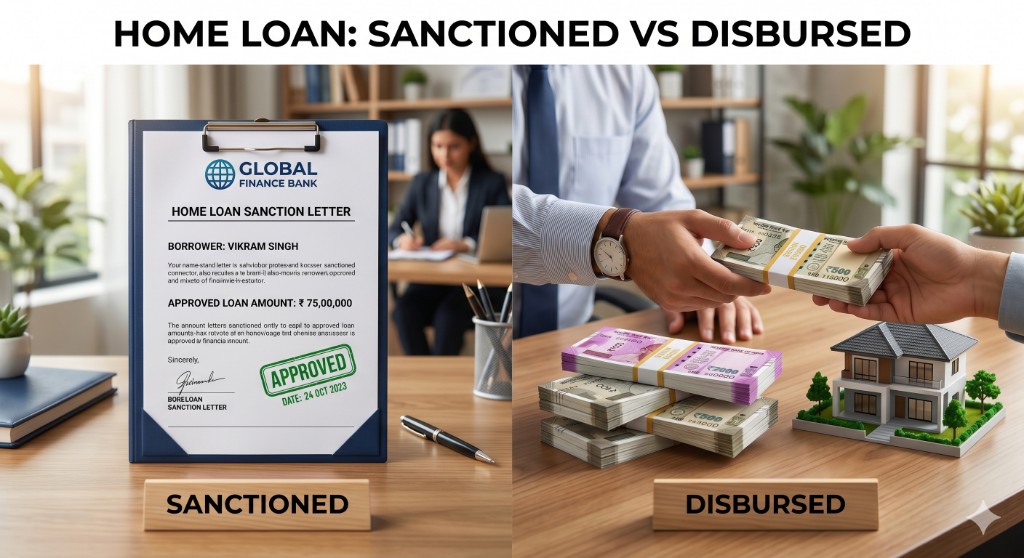

Sanctioned Amount

Maximum limit approved by lender based on profile, repayment capacity, and property eligibility. It is an approved ceiling, not immediate cash.

Example: Rs 75,00,000 approved

Disbursement Stage

Disbursed Amount

Actual funds transferred to your account or directly to seller/builder after conditions and deductions.

Example: Rs 71,50,000 released

This distinction is especially critical for under-construction homes, where release is milestone-based. Planning around realistic disbursement, not just sanction headline, is essential.

Feature-by-Feature Comparison

| Feature | Sanctioned Amount | Disbursed Amount | Key Insight |

|---|---|---|---|

| Definition | Maximum approved liability | Actual funds released | Defines approved ceiling vs actual borrowing |

| Timing | After verification and credit approval | After legal/property/disbursal checks | Approval phase and release phase are separate |

| Interest Basis | No interest before release | Interest starts on released amount | Interest follows actual drawdown |

| Amount Relationship | Always greater than or equal to disbursed total | Never exceeds sanctioned amount | Protects against over-lending |

| EMI Basis | Provisional estimate | Actual EMI on cumulative disbursed principal | Improves repayment realism |

| Processing Fee | Usually on sanctioned amount | No separate fee for release itself | Fee and release are not identical |

| Tax Benefit | No deduction on sanction alone | Deductions depend on actual borrowing/payments | Tax ties to real borrowing |

| Balance Transfer | New lender sanctions based on outstanding | Funds released to old lender | Enables refinancing migration |

| Cancellation | Possible within lender window | Cannot reverse after release | Exit is easier pre-disbursement |

| Credit Bureau | Shows approved limit | Shows live liability | Potential debt vs active debt |

What Creates the Gap Between Sanction and Disbursement?

💳

Processing Fees

Usually charged on sanctioned amount, reducing net amount received.

🔍

Legal & Technical Charges

Title checks and valuation verification can be deducted upfront.

📊

Valuation Variance

Lower lender valuation can reduce effective eligible release.

🔒

Insurance/Margin Adjustments

Bundled insurance or margin checks can reduce immediate payout.

🏗️

Construction-Linked Tranches

Funds are staged against certified progress.

👤

Profile Changes

Income/job/credit changes can trigger recalibration before release.

What Causes Disbursement Delays?

📋 Documentation quality

Mismatches or incomplete forms trigger follow-up loops.

⚖️ Legal verification completeness

Title chain and encumbrance checks can hold release.

🏠 Property valuation accuracy

Material value mismatch may trigger additional review.

🏗️ Construction stage mismatch

Demand and site progress mismatch causes re-inspection.

💰 Margin money verification

Borrower equity verification can delay payout.

📅 Seasonal load/rate lock expiry

High-volume periods and expired validity windows cause delays.

When a Loan Is Sanctioned but Never Disbursed

A sanction letter is not an unconditional release promise. In practice, many post-sanction triggers can pause or stop payout.

| Cause | What Happens | Resolution Path |

|---|---|---|

| Title defect discovery | Post-sanction legal issues found | Rectification/legal resolution may be needed |

| Builder risk reclassification | Developer risk category changes | Borrower may need alternate lender |

| Employment disruption | Repayment profile reassessed | Updated income proof required |

| Credit deterioration | Risk systems trigger review | Profile correction before release |

| Valuation variance | LTV breach reduces eligibility | Higher borrower contribution required |

| Regulatory approval issues | Project compliance concerns | Re-validate approvals |

| Internal lender holds | Portfolio or audit freeze | Formal escalation needed |

| Document authenticity concerns | Verification flags | Source-level revalidation required |

| Construction delays | Milestones not achieved | Release waits for certified progress |

| Insurance non-compliance | Mandatory conditions pending | Fulfill policy requirements |

What to Do If Your Loan Stays Undisbursed

- Engage your relationship manager immediately and ask for precise pending conditions.

- Insist on written explanation, not only verbal updates.

- Escalate through grievance/nodal channels when required.

- Resolve legal, valuation, documentation, or income gaps quickly.

- Evaluate parallel alternatives if delays exceed practical thresholds.

- Do not make seller commitments based on sanction alone.

Types of Disbursement in Home Loans

| Method | How It Works | Best For | EMI/Interest Impact |

|---|---|---|---|

| Lump Sum | Full eligible release in one shot | Ready-to-move/resale | Full EMI starts immediately |

| Construction-Linked | Milestone-based release | Under-construction/self-build | Interest on released tranches |

| Instalment/Staged | Predetermined stage release | Under-construction | Pre-EMI until full release |

| Direct Builder Payment | Funds sent to developer | New booking | EMI depends on release stage |

| Reimbursement | Borrower spends first, lender reimburses | Renovation/interiors | EMI tied to reimbursement timing |

| Escrow-Managed | Controlled release via escrow | High-value/risk-sensitive | Can add verification delays |

| Moratorium-Linked | EMI deferred for period | Selective schemes | Interest accumulates meanwhile |

| Subsidy-Adjusted | Subsidy reduces effective principal | Govt-linked schemes | EMI on net funded amount |

| Balance Transfer | New lender repays old lender | Refinance cases | New EMI starts at transfer |

Sanctioned Amount vs Current Outstanding Balance

After disbursement, a third number becomes critical: current outstanding balance. It is separate from sanction and original payout.

Set at Sanction

Rs 75,00,000

Usually static unless restructured/topped up; used for references and fee calculations.

Changes Every EMI

Rs 58,23,400

Dynamic outstanding reduces with EMI payments; interest is calculated on this active balance.

Tracking outstanding balance helps prepayment decisions, balance transfer timing, and interest optimization.

What a Sanction Letter Actually Contains

Home Loan Sanction Letter - Sample 2026

IllustrativeEven with sanction, release remains contingent on legal clearance, valuation, margin confirmation, and registration completion.

Quick EMI Calculator

Based on disbursed amount, not sanctioned amount

Disbursed Amount: Rs 50L

Interest Rate: 8.5%

Tenure: 20 years

Monthly EMI

Rs 43,391

For a live calculation using your own loan amount, rate, and tenure, use the home loan EMI calculator.

In This Guide

Top Lenders on Easiloan

Related Guides

How to Get Your NOC After Home Loan Closure

25 March 2026

What Are Secured Loans and How Do They Work?

11 May 2026

Risks of Taking a Loan Against Stocks

7 May 2026

Know Your Real Borrowing Capacity Before You Apply

Understanding sanction vs disbursement is the first step. Next is comparing lenders on actual release behavior and terms for your property profile.